The cloud wars of the last decade were defined by the race for infrastructure dominance—who could build the fastest data centers and offer the most reliable storage. Today, that battle has shifted layers. The new theater of war is the application layer, specifically the rapidly maturing ecosystem of AI agents.

According to new partnership data from CB Insights, the "Big Three" hyperscalers—Google, Microsoft, and Amazon—are no longer fighting for general-purpose dominance. Instead, they are aggressively carving out specialized territories. The data reveals a clear, emerging split: Google is winning the war for the developer’s mind, Microsoft is fortifying its moat around regulated enterprise industries, and Amazon is leveraging its infrastructure DNA to dominate the autonomous customer service sector.

The Landscape: Moving Beyond the Stack

For the past two years, the Big Three have inked 95 strategic partnerships with AI agent startups. These alliances are not merely marketing exercises; they are indicators of where these tech titans believe the highest growth—and the deepest stickiness—will materialize in the next five years.

The market for AI agents is evolving from simple, scripted chatbots into complex, autonomous entities capable of writing code, resolving high-stakes legal queries, and managing end-to-end healthcare workflows. As these agents become the primary interface for enterprise operations, the hyperscaler that hosts them wins the "cloud tax" of the future.

Chronology of the Shift

The transition from infrastructure competition to application-layer capture has unfolded in three distinct phases:

- 2023: The Infrastructure Land Grab. Following the surge in generative AI, hyperscalers focused primarily on securing GPU capacity and foundational model exclusivity (e.g., Microsoft’s deal with OpenAI and Google’s investment in Anthropic).

- Early 2024: The Proliferation of AI Startups. As foundational models became more accessible, an explosion of "agentic" startups appeared, focusing on specific functional tasks like code generation and customer service automation.

- 2025–Present: The Strategic Partitioning. Recognizing that infrastructure alone was insufficient for long-term retention, hyperscalers began forming deep product integrations and exclusive partnership clusters with these startups, effectively locking them into specific cloud environments through workflow and compliance advantages.

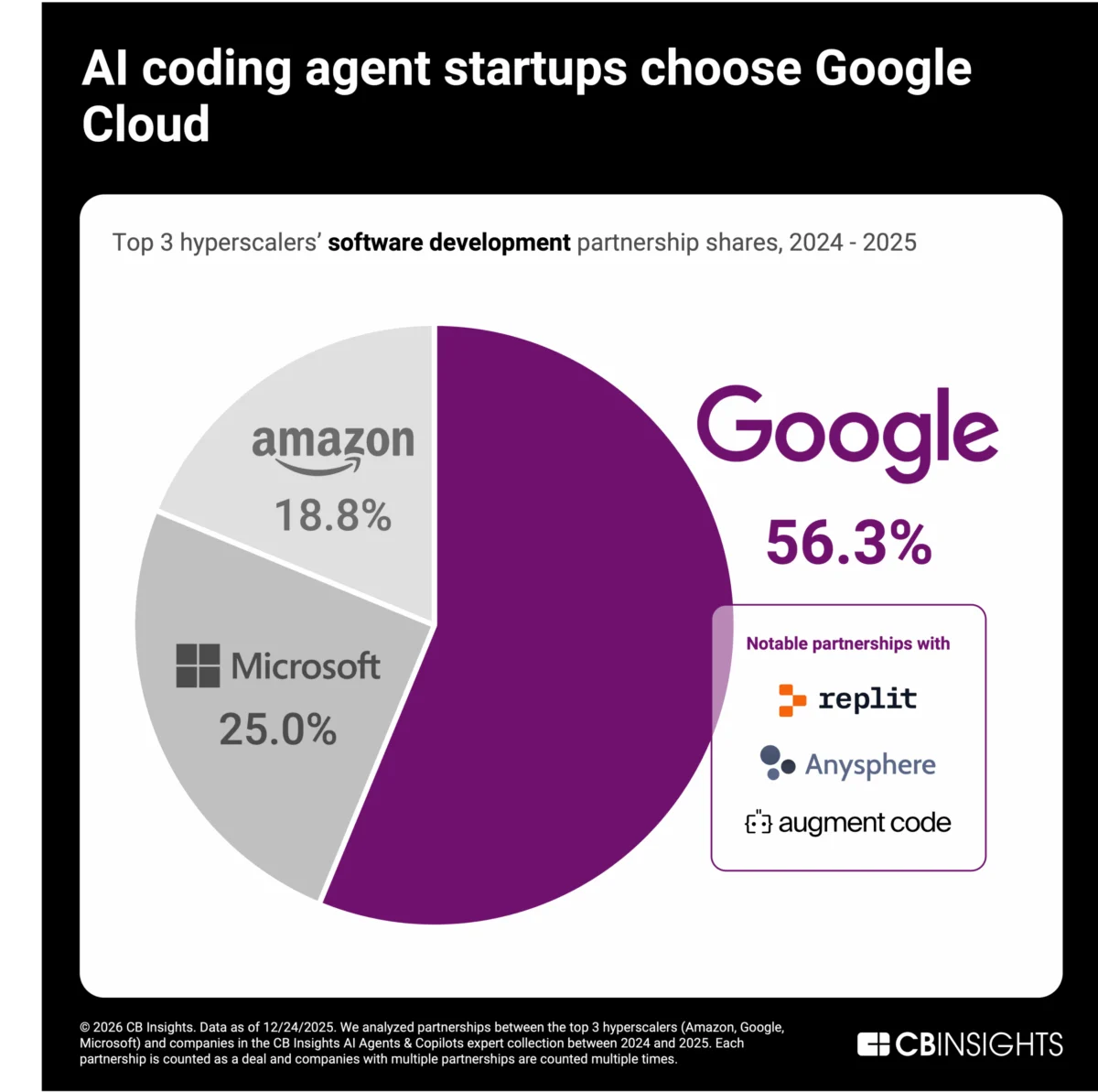

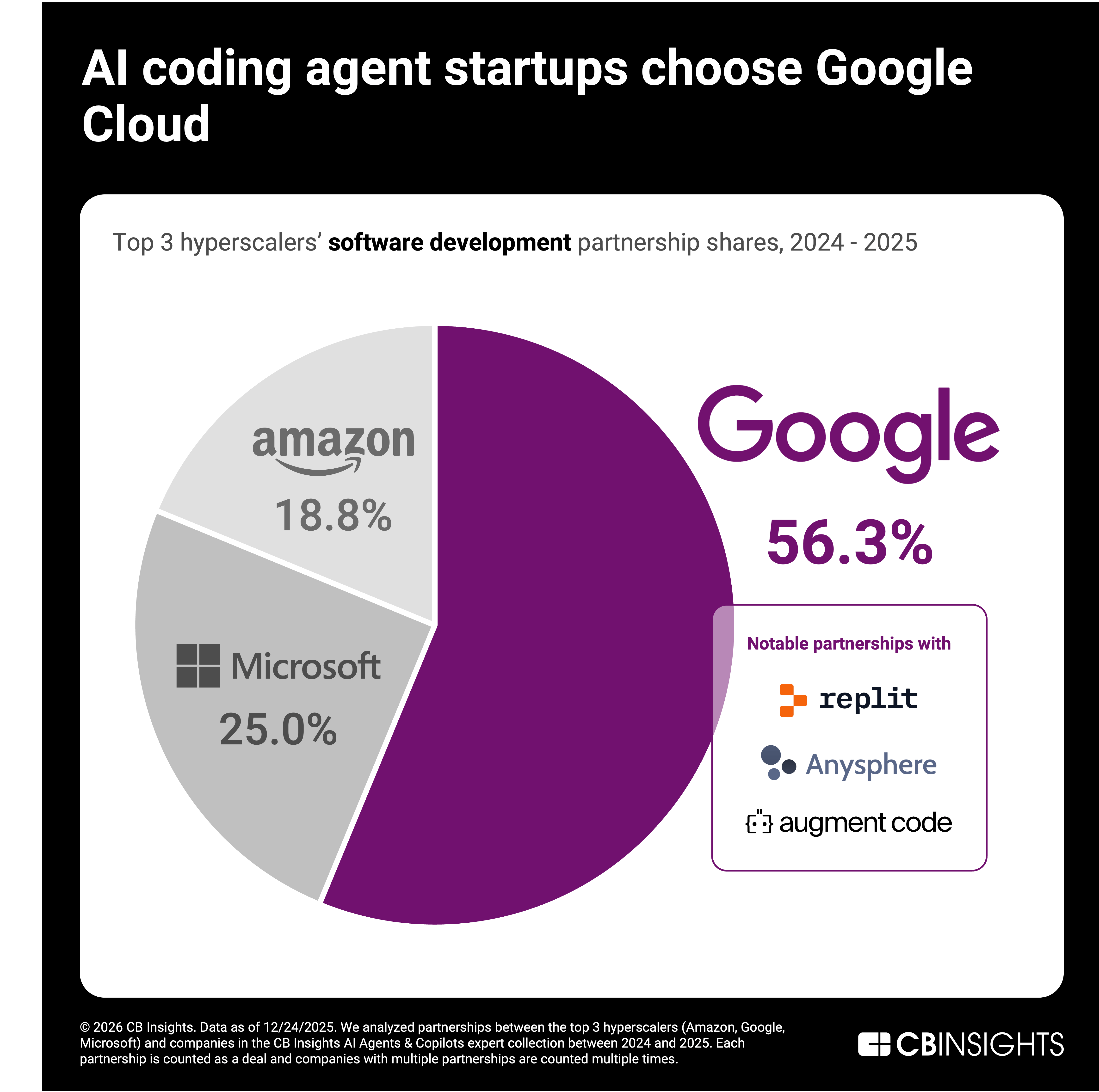

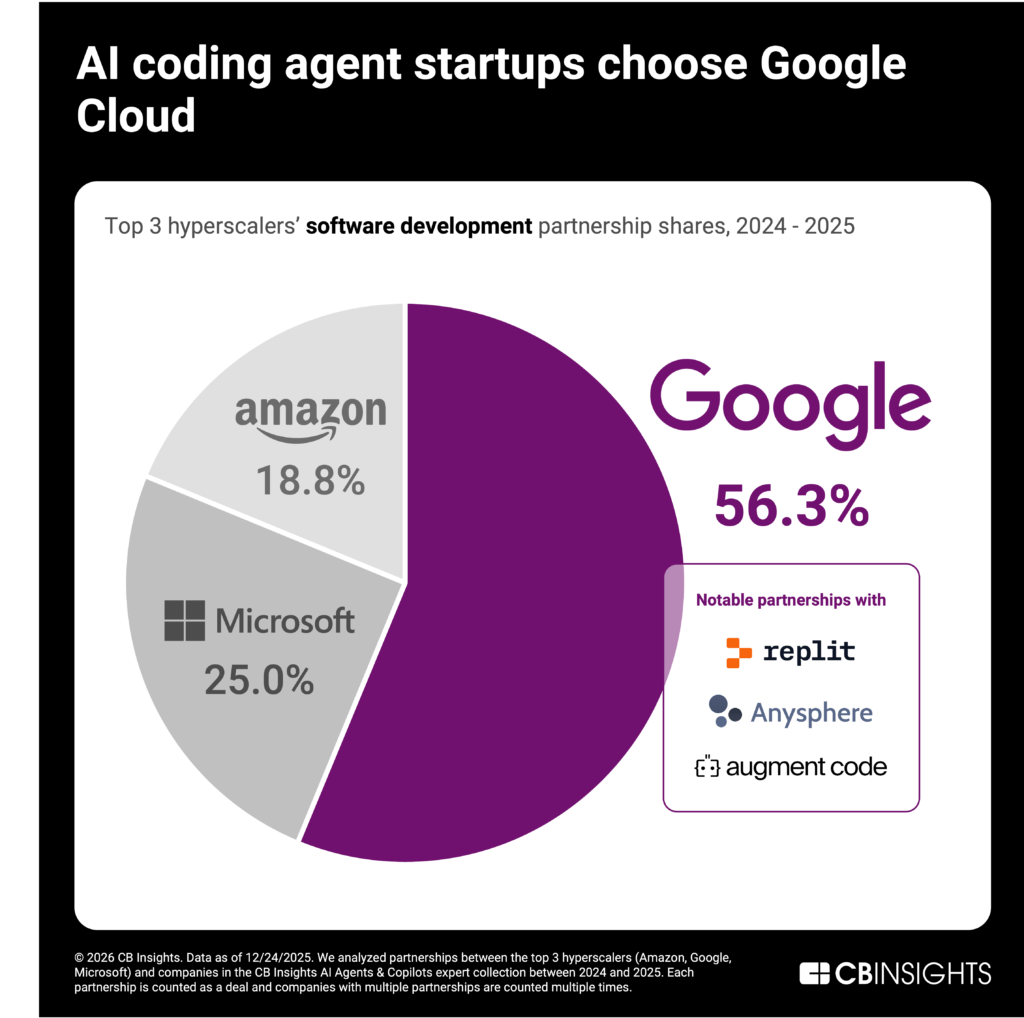

Google’s Strategy: Capturing the Developer Frontier

In the realm of horizontal AI agents, Google has established a commanding lead in software development, capturing 57% of all developer-focused AI partnerships.

Why Google Wins Developers

Google’s dominance in the coding sector is rooted in a fundamental shift in enterprise procurement: at developer-first companies, engineers make the infrastructure choices, not centralized IT procurement teams. Google has successfully leaned into this by offering a combination of high-performance Gemini models, seamless workflow integrations, and a long-standing commitment to open-source credibility.

The results are visible in the market: giants of the new AI-coding era, such as Anysphere (which recently reached $1B in ARR), Replit ($240M ARR), and Harness, have increasingly aligned with Google Cloud. By positioning itself as the "native" home for AI-assisted coding, Google ensures that as these startups scale, their underlying workloads remain on Google’s infrastructure.

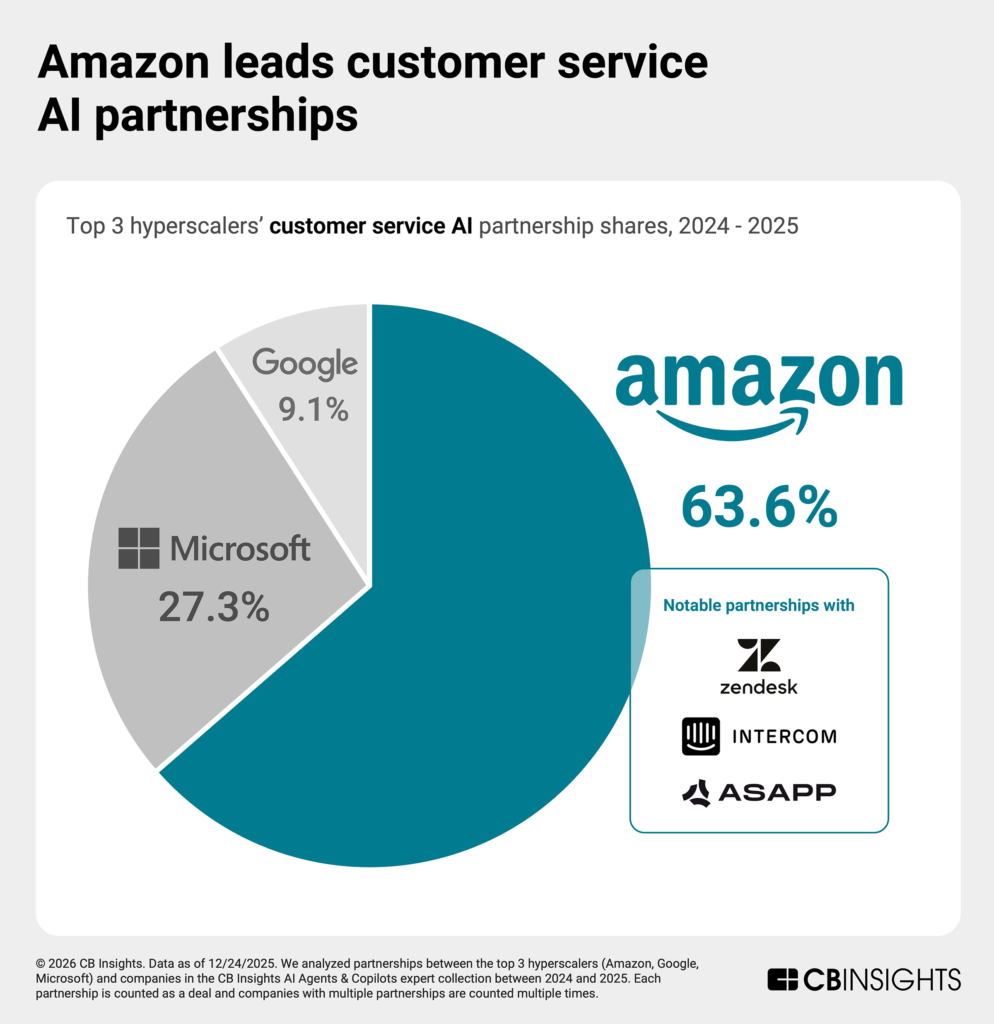

Amazon’s Strategy: The Infrastructure of Customer Service

While Google targets the technical elite, Amazon is playing to its historical strength: massive, real-time data processing. Amazon currently controls 64% of the customer service AI agent market, a sector that reached $1.6B in 2025.

The Power of "Amazon Connect"

Customer service AI is a high-stakes, low-latency environment. It requires the ability to process voice, chat, and CRM data in real-time. AWS, with its massive footprint and the established Amazon Connect ecosystem, provides a natural advantage that its rivals struggle to match.

Companies like Zendesk, Kore.ai, and Intercom have crossed the $100M ARR threshold by leveraging this infrastructure. Amazon’s strategy here is to move beyond simple chatbots to fully autonomous "resolution agents." By providing the infrastructure that allows these agents to handle end-to-end transactions without human escalation, Amazon is cementing its role as the backbone of global commerce.

Microsoft’s Strategy: The Moat of Compliance

If Google owns the developers and Amazon owns the contact center, Microsoft has effectively captured the "regulated enterprise." With 77% of partnership share in the legal and healthcare sectors, Microsoft is using compliance as a strategic weapon to prevent client churn.

The Flywheel of Trust

Microsoft’s approach is defined by the "Copilot" distribution layer. By integrating startups directly into its enterprise ecosystem, Microsoft provides them with instant access to the world’s largest corporate client base.

In the legal field, Harvey’s $150M commitment to Azure over two years is a testament to the power of this integration. Similarly, in healthcare, the integration of RhythmX AI into Microsoft’s Dragon Copilot—which handles over 13 million patient encounters—creates a "flywheel of trust." Because Microsoft is already the incumbent for data privacy and regulatory compliance, startups that partner with them gain an immediate "seal of approval" that is nearly impossible for competitors to replicate.

Supporting Data: The Market Split

| Sector | Leader | Market Share (Partnerships) | Key Driver |

|---|---|---|---|

| Coding/Dev | 57% | Developer preference/Gemini | |

| Customer Service | Amazon | 64% | Real-time infra/Connect |

| Regulated/Legal | Microsoft | 77% | Compliance/Copilot distribution |

The data underscores a clear trend: the "generalist" cloud era is over. The next phase of the cloud war will be won by whoever can provide the most specialized, frictionless environment for these new agentic applications.

Official Perspectives and Market Implications

While the hyperscalers have not issued official "declarations of war" regarding these splits, their quarterly earnings calls and developer conference messaging reflect a clear strategy.

- Google’s focus on "the developer ecosystem" suggests a belief that if they win the creators of the software, they automatically win the software itself.

- Amazon’s focus on "customer experience and operational scale" highlights their view that AI is ultimately a tool for optimizing business processes.

- Microsoft’s focus on "enterprise trust and compliance" reinforces their historical position as the primary platform for the Fortune 500.

The Implications for AI Startups

For the founders and investors backing the next generation of AI agents, the implications are profound. Choosing a cloud provider is no longer just about pricing or compute credits; it is a strategic decision about which ecosystem offers the best "path to market."

A startup building a coding agent that chooses to host on a platform other than Google may find itself fighting an uphill battle for developer adoption. Conversely, a legal-tech startup that ignores the compliance-heavy, enterprise-ready infrastructure of Microsoft risks being locked out of the lucrative healthcare and legal sectors.

Conclusion: The Era of Strategic Specialization

The battle for the AI agent layer is, at its core, a battle for the "operating system" of the modern enterprise. As we move through the rest of the decade, the distinctions between Google, Microsoft, and Amazon will only sharpen.

We are witnessing the end of the "Big Three" as interchangeable utilities. Instead, we are seeing the rise of a trifurcated market where each player acts as a specialized foundation. Google is the workbench for the innovator, Amazon is the engine for the enterprise operator, and Microsoft is the fortress for the regulated institution. For the startups building in these spaces, the winners will be those who best align their product vision with the unique competitive DNA of their chosen hyperscaler.

As the AI agent revolution matures, these early partnership clusters will likely harden into permanent industry standards. The hyperscalers have made their bets; now, the market will decide who successfully translates those partnerships into the long-term dominance of the next computing era.