Manufacturing is undergoing its most profound transformation since the introduction of the assembly line. For decades, the factory floor was dominated by "dumb" automation—fixed, purpose-built machines capable of performing a single, repetitive task with high precision but zero flexibility. Today, that paradigm is collapsing.

The convergence of artificial intelligence, advanced sensory arrays, and sophisticated mechanical engineering is giving rise to a new generation of robotics. These machines are not merely executing code; they are learning, adapting, and coordinating across complex, unpredictable environments. As over $1.2 trillion in new manufacturing investment floods the U.S. sector for 2025, the industry is transitioning from rigid automation to fluid, intelligent autonomy.

Main Facts: The Shift Toward General-Purpose Robotics

The modern manufacturing floor is no longer a static grid of conveyor belts and welding arms. It is becoming an interconnected ecosystem. The primary driver of this evolution is the integration of generative AI and computer vision into robotic systems, allowing them to perceive their surroundings and make real-time adjustments.

Key advancements include:

- Industrial Humanoids: Designed to integrate into human-centric workflows, these robots mimic human range of motion and dexterity, allowing them to operate in environments built for people without requiring costly retrofitting of infrastructure.

- Quadrupeds and Mobile Manipulators: These systems offer unprecedented mobility, navigating uneven terrain, climbing stairs, and reaching into confined spaces where traditional rail-mounted robots cannot function.

- Cognitive Coordination: Modern systems utilize edge computing to communicate with one another, optimizing throughput and identifying bottlenecks without human oversight.

The competitive landscape is shifting. Success is no longer defined solely by mechanical durability but by the seamless integration of hardware, proprietary software stacks, and AI models that improve with every cycle.

Chronology: The Road to Autonomy

To understand the current surge in manufacturing robotics, one must look at the historical trajectory of industrial technology:

Phase I: Rigid Automation (1970s–2000s)

The era of the "Industrial Robot." Companies focused on increasing speed and repeatability. These robots were fenced off from human workers for safety reasons and required specialized programming for every minor task change.

Phase II: The Collaborative Era (2010–2020)

The introduction of "cobots." Sensors and force-limiting software allowed robots to operate alongside humans safely. While more flexible than their predecessors, these machines still relied on human-led programming and structured environments.

Phase III: The AI Integration (2021–2024)

Large Language Models (LLMs) and vision-language models began to permeate robotics. Machines gained the ability to understand natural language instructions and visual cues. Instead of "coding" a robot, operators began "teaching" it through demonstration or simulation.

Phase IV: The Autonomous Renaissance (2025–Present)

The current era is defined by the massive $1.2 trillion capital injection into U.S. manufacturing. Facilities are now being designed from the ground up as "digital twins," where AI-driven robots handle end-to-end logistics, assembly, and quality assurance with minimal human intervention.

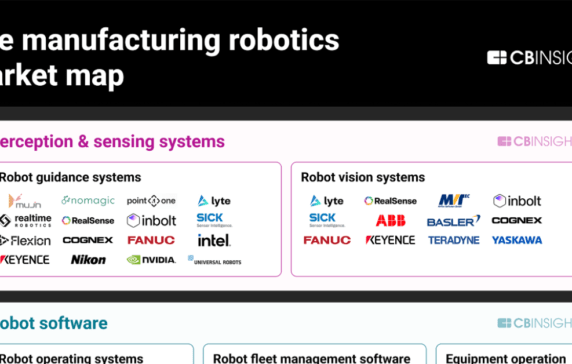

Supporting Data: Mapping the Market

The current market environment is highly fragmented but rapidly maturing. A comprehensive mapping of 116 companies across 14 distinct manufacturing robotics markets highlights the intensity of the current race.

Categorization Criteria

To identify the most viable players, analysts have employed "Mosaic" scoring—a metric that evaluates companies based on financial health, market momentum, and technological maturity. Companies with scores exceeding 700 are currently leading the charge, while major corporations are being tracked based on their aggressive M&A activity and strategic R&D partnerships.

| Market Segment | Primary Focus |

|---|---|

| Humanoid Assembly | Dexterity and ergonomic integration |

| Mobile Logistics | Autonomous transport and warehousing |

| Vision Systems | Real-time quality control and spatial awareness |

| Edge AI Controllers | Low-latency decision-making at the machine level |

The data indicates that the "winners" in this space are those that prioritize "full-stack" integration. Companies that rely solely on hardware are finding themselves commoditized, while those that provide the "brain" for the machine—the software and AI layer—are commanding significant market premiums.

Official Responses and Industry Sentiment

Industry leaders and policy makers have expressed a unified sentiment: the transition to autonomous manufacturing is a geopolitical necessity.

In a recent industry forum, a spokesperson for a leading global industrial robotics firm noted: "The narrative has shifted from ‘robots replacing jobs’ to ‘robots securing competitiveness.’ With the $1.2 trillion in new facility investments announced in 2025, our clients are not trying to eliminate the human element; they are trying to solve for labor shortages and supply chain fragility. The autonomy provided by AI allows for domestic manufacturing to become cost-competitive with overseas markets for the first time in decades."

Conversely, labor advocates emphasize the need for "upskilling." As the demand for manual assembly decreases, the demand for "robot fleet managers"—technicians capable of monitoring, maintaining, and refining the AI models—has spiked. The consensus among the manufacturing elite is that the workforce of 2030 will look fundamentally different, requiring a blend of mechanical aptitude and digital literacy.

Implications: The Future of the Global Supply Chain

The implications of this shift are far-reaching, affecting everything from international trade policy to the architectural design of cities.

1. Reshoring and "Hyper-Local" Manufacturing

As autonomous systems drive down the cost of production, the economic argument for offshoring to low-wage countries weakens. We are entering an era of "hyper-local" manufacturing, where facilities located near consumer hubs can rapidly adapt to demand shifts, drastically reducing shipping times and carbon footprints.

2. The Rise of the "Software-Defined Factory"

Just as the automotive industry is shifting to "software-defined vehicles," the factory floor is becoming a software-defined asset. Manufacturers can now "download" new capabilities to their robotic fleets. If a product design changes, the facility doesn’t need to be gutted; it simply needs a software update to reconfigure the robotic workflows.

3. Safety and Ethics

With the removal of human oversight comes the challenge of safety in autonomous environments. Current regulatory frameworks are struggling to keep pace with robots that learn on the job. Establishing "algorithmic accountability" will be the next major hurdle for both corporations and government agencies.

4. Economic Concentration

There is a risk that the benefits of this transformation will accrue primarily to the top 1% of firms capable of making the massive capital investments required. The $1.2 trillion in investment is concentrated in facilities that require high-speed connectivity, sophisticated energy grids, and deep-tech talent pools. Smaller manufacturers may find themselves locked out of this ecosystem unless modular, "robotics-as-a-service" (RaaS) models become more prevalent.

5. Sustainability and Circularity

Autonomous robotics are uniquely suited for the circular economy. Disassembling old products for parts and recycling is a complex, unpredictable task that human labor finds tedious. Intelligent robots, equipped with high-resolution vision systems, can identify, sort, and disassemble goods at scale, turning waste streams into high-value raw materials.

Conclusion: The Path Forward

The integration of AI into manufacturing robotics is not merely a technical upgrade; it is a structural redesign of how humanity produces goods. The companies that will dominate the next decade are those currently investing in the intersection of hardware, software, and data.

As we move through 2025 and beyond, the focus will shift from the "novelty" of seeing a humanoid robot on a factory floor to the "utility" of those machines performing millions of safe, autonomous cycles. The $1.2 trillion in investment is a massive vote of confidence in the future of intelligent automation. For the manufacturers of the future, the choice is clear: adapt to the era of the autonomous factory, or risk obsolescence in an increasingly efficient global market.

The era of the "dumb machine" has ended. The era of the intelligent, adaptive, and autonomous industrial ecosystem has officially begun. Whether this leads to a new golden age of manufacturing productivity will depend on the speed at which these 116 mapped companies—and the broader industry—can solve the remaining challenges of scalability, safety, and workforce integration.